In a recent New York Times column, economist Paul Krugman once again took to chastising a claim he has infamously dubbed the “confidence fairy.” According to the Nobel laureate, the “confidence fairy” is the erroneous belief that ambiguity over future government regulation and taxation plays a significant role in how investors choose to put capital to work. To Krugman, the anemic economic recovery in the United States shouldn’t be blamed on this “uncertainty” but rather a “lack of demand for the things workers produce.” Being the most prominent mouthpiece for Keynesian economic policy in modern times, the Princeton professor represents the school’s circular thinking very well. Keynes and his followers saw most economic slumps as being the result of insufficient spending. A slowdown in spending means the animal spirits aren’t so aggressive in their lust for immediate consumables.

As a thinker, Keynes viewed a preference for saving over spending as ignorant and asinine. In his essay “Economic Possibilities for our Grand Children,” he belittled the “purposiveness” of misers who are forever looking toward the future instead of relishing in the present. The man who behaves with a purpose is “always trying to secure a spurious and delusive immortality” while depriving those around him of his wealth. This is the heart of Keynesianism. Saving is seen as a necessary evil while instant gratification is looked down upon as morally repugnant. Keynes was a hater of bourgeoisie prudence throughout his professional career. It is likely that this antagonism played a role in the development of his theories on economics.

But even assuming that Keynes took the value-free, deductive approach to economic science, the view of spending as the driving force of improved living standards is still horribly inaccurate. Human beings possess infinite wants. So, in a sense, there is never a true lack of demand; just the resources to fulfill desire. And these resources are not something to conjure up out of thin air. They must first be produced. As Henry Hazlitt explains,

…demand and supply are merely two sides

of the same coin. They are the same thing looked at from different

directions. Supply creates demand because at bottom it is demand.

Goods and services are what ultimately enhance human life. Without

them, man would still be relegated to live as a nomad desperately

seeking out food each and every day. It is through producing, saving,

and investing that the eternal scarcity of the world becomes

increasingly manageable. In other words, the act of producing more than

is immediately consumed is what saves humanity from a hand-to-mouth

existence. This improved material well-being can then lend itself to

further spiritual pursuits. Murray Rothbard recognized the necessity of

available resources for less-material purposes when he wrote:

All great works of art, great emanations

of the human spirit, have had to employ material objects: whether they

be canvasses, brushes and paint, paper and musical instruments, or

building blocks and raw materials for churches. There is no real rift

between the “spiritual” and the “material” and hence any despotism over

and crippling of the material will cripple the spiritual as well.

As a species, we are forever trying to achieve a happiness dictated

solely by our own individual valuations. This requires labor and

production in order to meet whatever ends are sought. With this truth

in mind, it becomes clear that economies don’t necessarily suffer from

an absence of demand but really a lack of investment or production.

Since there are always needs to be fulfill, an uninhibited market

economy would never undergo a period of long-term unemployment. There

would be capital to be worked and put into use. So what then causes

entrepreneurs and capitalists to withhold investment?In a landmark article in The Independent Review, economic historian Robert Higgs presented evidence that the Great Depression was not prolonged by a slack in demand but rather the unprecedented intervention into private life by the Roosevelt regime. Titled “Regime Uncertainty: Why the Great Depression Lasted So Long and Why Prosperity Resumed after the War,” Higgs summarizes his position:

First, the Great Depression was not just

another economic slump. In depth and duration it stands far apart from

the next most severe depression in U.S. history, that of the 1890s. We

are talking about history, not physics; unique events may have unique

causes. Second, the hypothesis about regime uncertainty makes perfectly

good economic sense. Nothing in the logic of the explanation warrants

its dismissal or disparagement. Third, given the unparalleled outpouring

of business-threatening laws, regulations, and court decisions, the

oft-stated hostility of President Roosevelt and his lieutenants toward

investors as a class, and the character of the antibusiness zealots who

composed the strategists and administrators of the New Deal from 1935 t o

1941, the political climate could hardly have failed to discourage some

investors from making fresh long-term commitments. Fourth, there exists

a great deal of direct evidence that investors did feel extraordinarily

uncertain about the future of the property-rights regime between 1935

and 1941. Historians have recorded countless statements by

contemporaries to that effect; and the poll data presented earlier

confirm that in the years just before the war most business executives

expected substantial attenuations of private property rights ranging up

to “complete economic dictatorship.” Fifth, investors’ behavior in the

bond market attests in a striking way that their confidence in the

longer-term future took a beating that corresponds exactly with the

Second New Deal.

Much like the Great Depression, there is evidence abound to support

the notion that regulatory uncertainty is presently withholding the

private investment that is the true source of economic growth. The

newly released mid-year economic report

from the National Small Business Association shows that 34% of

small-business owners are expecting a sluggish economy on the horizon

while 68% of respondents cited economic uncertainty as the biggest

“challenge” to future productivity. In the September 2012 Small Business Optimism Survey

released by the National Federation of Independent Business, the

results showed a new record of 22% of respondents who view political

uncertainty as a leading cause of their reluctance to expand. Higgs

himself points out

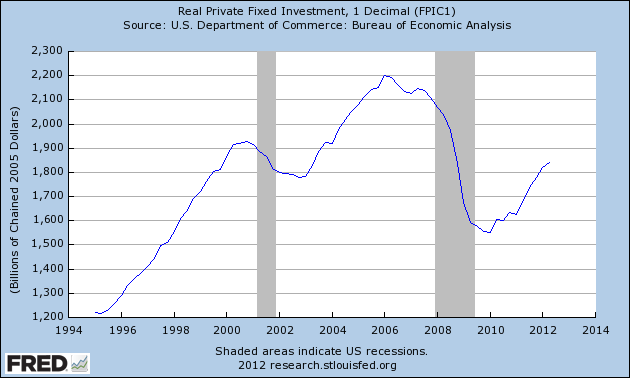

in a recent blog post that real private fixed investment has yet to

surpass its lowest point during the bust of the dot-com bubble.

Historically, economic downturns have been met with upswings that matched in terms of intensity. But at no other time since the Great Depression has the recovery been as weak as it is now. The explanation lies in the fact that something is causing investors to keep money on the sidelines rather than risk putting it towards satisfying the limitless wants of consumers. Empirical evidence and logic would suggest that it is the current atmosphere of tentative political measures that is frightening capitalists whose job it is to create wealth. From the unknown consequences of the Affordable Care Act and the Dodd-Frank financial regulatory bill to the expiration of the Bush-era tax cuts at the end of 2012, it is unclear as to the amount of income businessmen will be allowed to keep in the near future. As economist John B. Taylor shows, the amount of federal government workers engaged in regulatory activity has taken off since 2008.

Likewise, the number of expiring tax provisions has also increased substantially over the past four years.

Since man is endowed with free will, the future is never certain. Entrepreneurs and capitalists are never guaranteed a profit so they must invest with prudence if they hope to come out with more wealth in the end. The incessant meddling by the political class makes this process all the more difficult. There is little incentive to risk precious capital when it could be looted at any time. Political obscurity and a growing class of planners who take it upon themselves to forcefully engineer society in their own vision makes for an unhealthy business climate.

The theory which puts a lack of aggregate demand as being the cause of economic recessions has the issue backwards. Demand by itself doesn’t add to the stock of goods in society; only production does. Because economic theory deals with the interactions of mankind it needs to be applicable to all times and places. On a desert island, only a true charlatan would insist that a “lack of demand” is holding the primitive economy back from its full potential. Desert islands are no different from today’s economy; both are still dominated by scarcity. If the world economy is ever going to recover, the obstacles put in business’s place have to be lifted to make way for investment in real, tangible goods and services. Consumption will come after.

No comments:

Post a Comment